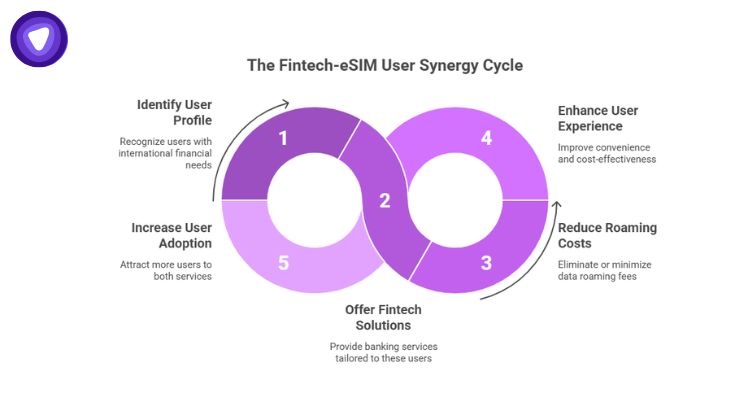

- Gap in Digital Banking: Wise, bunq, and digital nomad-focused neobanks have solved cross-border payments but left connectivity untouched. Bundling eSIM into premium tiers closes that gap and gives globally mobile users a single platform for both money and data abroad.

- Integration Models: Three integration models make this viable: allotment-based data inclusion, activation-triggered coverage tied to foreign card spend, and an in-app eSIM marketplace with preferential pricing for premium subscribers.

- Core Dependency: Mobile connectivity and digital banking are functionally inseparable for frequent travelers. Internet access is required for authentication codes, transaction approvals, and account management, making eSIM a natural extension of the banking product rather than an add-on.

- Retention Driver: eSIM bundling solves a core problem with premium tier design. Most perks are valued at signup and forgotten after. Data connectivity is used on every international trip, which reinforces card usage, strengthens retention, and feeds interchange revenue directly.

- Competitive Timing: The window to differentiate is open now but will not stay that way. Multi-currency accounts, fee-free ATM withdrawals, and travel insurance all followed the same pattern: early movers owned the behavior, late movers paid to match it. eSIM is at the start of that curve.

Wise, Bunq, and similar digital nomad-focused banks can bundle eSIM directly into premium tiers by including global data allowances, travel connectivity perks, or in-app eSIM activation as part of their paid plans.

The case for doing it is straightforward. Digital banks have already solved cross-border payments, multi-currency spending, and remote account access. Connectivity is the one piece still missing. Right now, customers entering a new country go through the same friction every time: sourcing a roaming plan, swapping a SIM, or buying a temporary data package. None of that touches the bank.

For internationally mobile users, mobile connectivity and digital banking go hand in hand. Internet access is essential for authentication, transactions, and account management. By including eSIM in premium tiers, banks provide a benefit customers use on every trip, increasing engagement and subscription value.

Why the Overlap Between Fintech Users and eSIM Users Is Not a Coincidence

The demographic profile of a Wise Premium or bunq SuperGreen subscriber and the profile of an eSIM power user are nearly identical: frequent international travelers, remote workers, freelancers paid across currencies, and professionals who operate across multiple jurisdictions.

GSMA Intelligence forecasts global eSIM smartphone connections will reach 4.9 billion by 2030, representing 55 percent of all smartphone connections. The adoption curve is steepest among younger, tech-comfortable users, exactly the segment neobanks have spent years and significant marketing budgets acquiring.

Bunq, which serves 12.5 million users across Europe, explicitly positions itself as the bank for digital nomads. Wise processed £118.5 billion in cross-border transactions in FY2024. These are not casual users occasionally traveling for vacation. These are people whose financial lives are structurally international, and who face data roaming fees as a recurring, predictable cost every time they cross a border.

That cost is not small. Roaming charges from traditional carriers can run $10 to $15 per day in many markets. For someone traveling 15 to 20 weeks per year, that adds up to hundreds of dollars annually, a line item that a premium banking tier could absorb or eliminate entirely.

What “Bundling” Actually Means in Practice

Bundling eSIM into a premium banking tier is not as simple as sticking a data plan into a welcome email. There are three distinct models fintechs can realistically pursue:

Model 1: Allotment-Based Inclusion

The bank negotiates a bulk data agreement with an eSIM provider and includes a fixed monthly data allotment as part of the premium subscription. Users activate the eSIM through the bank’s app. Think of it like how some premium cards include a streaming subscription, except the value is connectivity rather than content.

This model works best for banks with large, active premium user bases because the economics only make sense at volume.

Model 2: Activation-Triggered Coverage

Rather than providing always-on data, the bank triggers eSIM activation when a user’s card is charged abroad. The system detects a foreign transaction, provisions a local data profile for that country, and sends a push notification. The user gets connectivity from the moment they land, tied directly to their financial activity.

This is technically more complex. It requires API integration between the bank’s transaction processing layer and the eSIM management platform. But it is also the most seamless experience available to the end user.

Model 3: Marketplace + Preferential Pricing

The bank integrates an eSIM marketplace into its app and offers premium subscribers discounted rates. This is the lightest-touch approach and the fastest to implement, but it requires consistent margin sharing between the bank and the eSIM provider.

The Technical Integration Layer

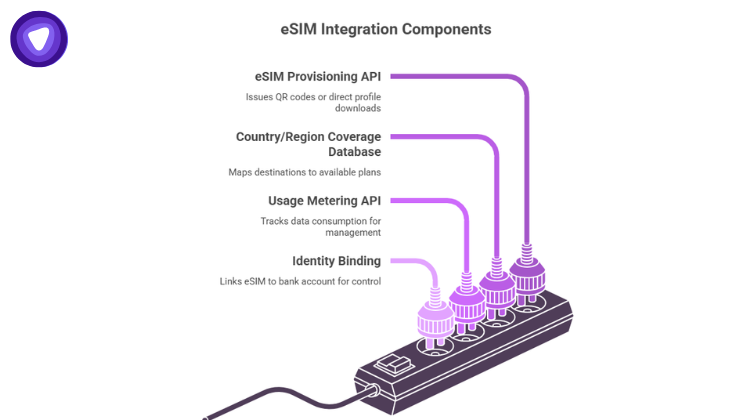

For any of these models to work, fintech needs access to an eSIM platform via API. The core components are:

- eSIM provisioning API: Issues QR codes or direct profile downloads to activate a data plan on a user’s device

- Country/region coverage database: Maps destination countries to available plans

- Usage metering API: Tracks data consumption so the bank can manage allotments or alert users approaching limits

- Identity binding: Links the eSIM profile to the bank account for a single point of control

Most modern eSIMs follow the GSMA RSP (Remote SIM Provisioning) standard, which means the provisioning side is largely standardized. What differentiates eSIM providers is coverage breadth, per-plan pricing, API reliability, and the quality of the dashboard tooling they provide to business partners.

The integration sits naturally alongside existing bank app infrastructure, particularly for neobanks that already handle push notifications, in-app card controls, travel notifications, and currency conversion features.

How This Changes the Premium Tier Economics

The average monthly cost of a premium neobank tier ranges from €7 to €17 across major European fintechs. At that price point, the value proposition has to be clear and immediate. Travel insurance and multi-currency accounts are strong anchors, but they are also widely replicated.

eSIM data is sticky in a way that most perks are not. Once a user activates an eSIM through their banking app, they associate that bank with staying connected abroad. That is a behavioral link that reinforces card usage internationally, which directly feeds interchange revenue for the bank.

| Feature | Traditional Premium Perk | eSIM Bundle |

| Perceived Value | High at signup, fades over time | High on every international trip |

| Usage Frequency | Occasional (insurance, lounge access) | Every trip abroad |

| Card Activation Link | Indirect | Direct (foreign spend triggers it) |

| Differentiation | Moderate (widely copied) | High (few banks offer it today) |

| Operational Cost | Fixed (contract-based) | Variable (per-use or allotment) |

| User Retention Signal | Weak | Strong (habitual activation) |

The economics improve further when the eSIM is tied to international card usage. Banks already earn interchange on foreign transactions. If the eSIM bundle increases the frequency and volume of those transactions, because the user is abroad more often and reaches for the card that also keeps them connected, the bundle more than pays for itself.

What the User Journey Looks Like

Imagine a freelance consultant who uses a premium neobank account. She lands in Seoul for a client meeting. Before her phone connects to a local tower, her banking app sends a notification: “You are in South Korea. Your plan includes 1 GB of local data. Tap to activate.”

She taps. Her phone is online within 30 seconds. She pays for her taxi from the airport using her bank card. She checks her balance, converts KRW to EUR, and messages her client, all on local data, with no SIM swap, no roaming charges, no hunting for a convenience store selling a prepaid card.

That experience is not futuristic. The technology to build it exists now. What has been missing is the commercial arrangement between banks and eSIM providers that makes it financially sensible to package.

Regulatory and Compliance Considerations

Fintechs operating across the EU, UK, and other regulated markets need to think carefully about how eSIM bundling interacts with their existing licensing structure.

Key questions to address before launch:

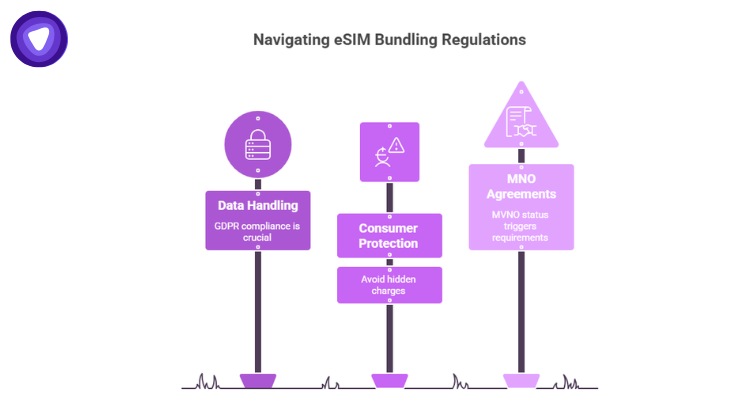

- Data handling: eSIM provisioning involves device identifiers (EID, ICCID). This data must be handled in compliance with GDPR or equivalent frameworks. Clear disclosure in the privacy policy is non-negotiable.

- Consumer protection: If the eSIM allotment runs out mid-trip, users need clear notification before they incur out-of-plan costs. Regulators in the EU have become increasingly attentive to hidden charges in digital financial products.

- MNO agreements: In some markets, the bank becomes a de facto MVNO (Mobile Virtual Network Operator) if it resells connectivity under its own brand. This may trigger additional regulatory requirements depending on jurisdiction.

Working through an established eSIM provider rather than building direct MNO relationships sidesteps most of these issues. The provider handles the carrier-layer compliance, and the bank simply surfaces the product to its users.

PureVPN eSIM: Built for the Partner Model

For fintechs looking to move from concept to live product, the partnership layer matters as much as the technology. PureVPN eSIM offers coverage across 150+ countries with a straightforward API model designed for business integrations. The plans are structured for flexibility, so fintechs can offer single-country plans, regional bundles, or global passes depending on how they design their premium tier.

The business model supports white-label or co-branded deployments, which means a neobank can surface eSIM data plans under its own product identity rather than pushing users to a third-party app. That continuity matters for retention.

The user stays inside the bank’s ecosystem for the entire travel connectivity experience. PureVPN eSIM also sits alongside PureVPN’s broader security infrastructure, which is relevant for users who value both connectivity and data privacy while accessing financial services on public networks abroad.

The Window Is Narrow

Neobanks thrive by being first to a valuable feature set, then defending that position before incumbents and competitors catch up. Multi-currency accounts were a differentiator in 2016. Fee-free international ATM withdrawals followed. Travel insurance bundles became standard. The pattern repeats.

eSIM bundling is at the beginning of that cycle. The fintechs that integrate it into premium tiers now will own the narrative and the user behavior before it becomes table stakes. The technology is ready. The user demand is documented. The only question is which bank moves first.