- Embedded finance has moved beyond banking. Non-financial platforms now process trillions in transactions, with the US market alone projected to hit $7 trillion by 2026, making security a product responsibility, not just a compliance task.

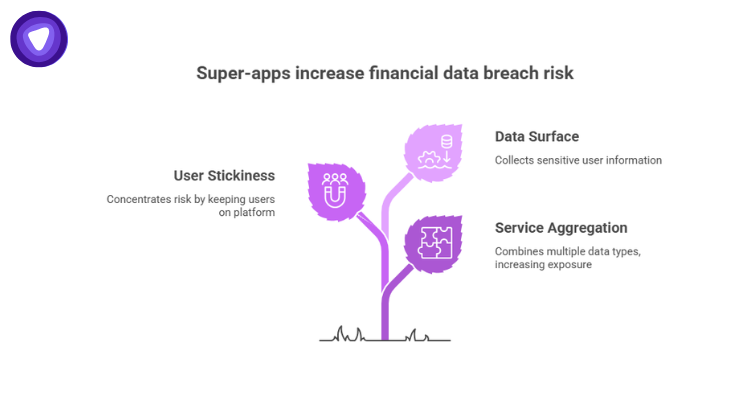

- Super-apps create concentrated risk. By aggregating payments, identity, lending, and behavioral data in one place, a single breach carries compounded exposure across every data class the platform holds.

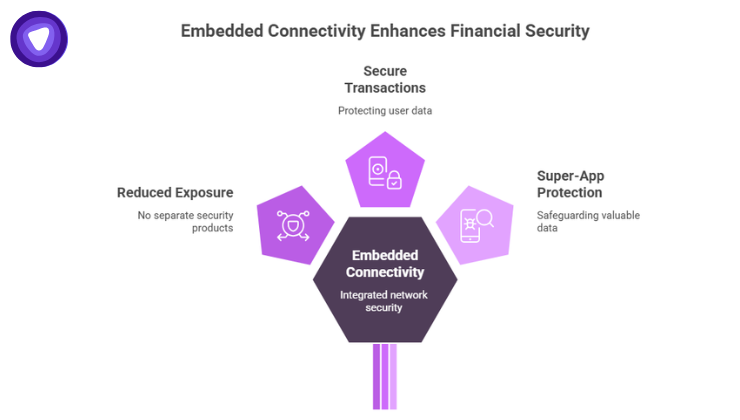

- Embedded connectivity is a distinct infrastructure layer. Integrating encrypted tunneling and VPN capabilities directly into a platform reduces network-layer attack surface without requiring users to take any action.

- The white-label model solves the build-versus-buy problem. Fintech platforms can embed enterprise-grade connectivity under their own brand without maintaining VPN servers, managing certificates, or tracking protocol changes.

- Security built into architecture outperforms security bolted on top. Platforms that treat the network layer as a foundation rather than an afterthought are better positioned for regulatory compliance, user trust, and breach resilience.

GrabPay processed over $2.5 billion in annualized payment volume while simultaneously offering insurance, lending, and investment products to users who never once opened a banking app. Grab is not a bank. It is a super-app that absorbed financial services into its core infrastructure. That outcome is embedded finance operating at scale, and it is already the norm in Southeast Asia, Brazil, and several other high-growth markets.

What is less discussed is the second infrastructure shift running in parallel: embedded connectivity. The security layer is no longer a standalone enterprise product. It is becoming part of the platform itself.

When these two forces converge, the question for every fintech, BaaS provider, and super-app operator is the same: who is responsible for the pipe that the money moves through?

What Embedded Finance Actually Means in 2026

Embedded finance is not about banks going digital. It is about non-financial companies becoming the place where financial transactions happen.

A logistics platform offering fleet insurance. A B2B SaaS tool with built-in invoice financing. A retail app with buy-now-pay-later baked directly into checkout. These are not edge cases. The embedded finance market is on track to exceed $7 trillion in transaction value in the US alone by 2026, up from roughly $2.6 trillion in 2021.

The mechanism behind this is mostly invisible to end users. Banking-as-a-Service (BaaS) providers, payment APIs, and modular compliance tooling have made it technically straightforward for any company with a user base to offer financial products. The regulatory and security burden, however, has not become straightforward at all.

Embedded Connectivity: The Layer Nobody Talks About

While embedded finance continues to dominate industry conversations, another infrastructure trend is quietly gaining importance: embedded connectivity. It refers to integrating network security, VPN tunneling, or private connectivity directly into a product rather than offering security as a separate enterprise tool.

As more financial services become embedded into everyday applications, connectivity becomes a critical part of protecting transactions, user data, and platform infrastructure.

Key characteristics of embedded connectivity include:

- Integrating network security directly into a platform instead of relying on standalone security tools.

- Embedding VPN tunneling and private connectivity within consumer and business applications.

- Providing secure Wi-Fi protection as a native feature inside consumer banking apps.

- Enabling white-label VPN and zero-trust access capabilities within B2B SaaS platforms.

- Reducing network-layer exposure without requiring users to manage separate security products.

- Supporting the growing security needs of applications that process payments, store financial data, or offer lending services.

- Helping super-apps protect increasingly valuable combinations of payment, identity, and behavioral data.

- Treating connectivity as a foundational security layer rather than an add-on feature.

Why Super-Apps Are the Pressure Point

The super-app model, dominant in Southeast Asia and increasingly tested in Western markets, accelerates this convergence in ways that traditional app architecture was never designed to handle.

A super-app aggregates services: payments, lending, insurance, logistics, healthcare, and communications inside a single platform. The user never leaves. That stickiness is the business model. But from a security architecture standpoint, that same stickiness creates a concentration of risk that traditional app segmentation was designed to avoid.

The data surface is substantial. A super-app knows where users live, where they work, what they buy, what they earn, who they pay, and increasingly, what their health looks like. When financial services sit on top of that data, the security stakes are not incremental. They are categorical.

According to IBM’s Cost of a Data Breach Report, the average cost of a financial services data breach reached $6.08 million, which is 22% higher than the global average and the second highest of any industry. Super-apps, by aggregating multiple data classes into one platform, face compounded exposure across every one of those categories.

The Embedded Connectivity Fintech Stack: What It Looks Like

For any platform at the intersection of finance and aggregated services, the security architecture needs to move from perimeter-based thinking to continuous, embedded protection. Here is how that stack typically breaks down:

| Layer | Function | Embedded Solution |

| Network Security | Encrypt data in transit, mask IP | White-label VPN / encrypted tunneling |

| Identity & Access | Verify users, manage sessions | Embedded IAM with MFA |

| Data Residency | Comply with local data laws | Geo-routing via VPN infrastructure |

| Threat Detection | Monitor anomalous behavior | API-integrated security monitoring |

| Endpoint Trust | Ensure device integrity | Zero-trust network access (ZTNA) |

| Compliance | Meet PCI-DSS, GDPR, local regs | Audit logging, encrypted channels |

The embedded connectivity fintech layer sits at the foundation. It is the encrypted pipe through which all of these other functions operate. Without it, every other security investment becomes more fragile.

Three Real Problems Embedded Connectivity Solves in Fintech

Each of these problems is active, not theoretical. Fintech platforms operating across multiple markets are dealing with all three right now.

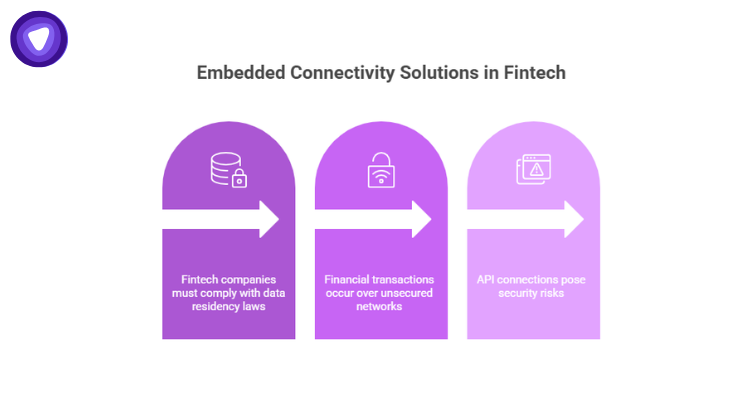

1. Regulatory Data Localization

Fintech companies operating across multiple jurisdictions face a complex set of data residency requirements. GDPR in Europe, PDPA in Southeast Asia, and sector-specific rules in markets like India and Brazil all demand that certain financial data stay within geographic boundaries.

Embedded VPN infrastructure with geo-routing capabilities lets platforms route traffic through compliant data corridors by default. The compliance is not bolted on after the fact. It runs at the infrastructure level.

2. Public Network Exposure for Financial Transactions

A significant share of mobile financial transactions still happen over unsecured or semi-trusted networks. Coffee shops, airports, co-working spaces. Users accessing embedded financial services from these environments are exposed to interception risks that encryption-in-transit alone does not fully address.

Embedded connectivity solves this by creating a protected tunnel that activates for financial operations, without requiring user action. The user does not need to know a VPN is running. It simply is.

3. Partner and Third-Party API Risk

Embedded finance, by design, involves dozens of third-party integrations: BaaS providers, card networks, KYC vendors, fraud detection tools. Each API connection is a potential entry point. Embedded connectivity tools that enforce encrypted, authenticated connections for all third-party calls dramatically reduce the lateral movement risk if any one integration is compromised.

The White-Label Opportunity Nobody Is Pricing In

For platforms that want to offer embedded connectivity as a feature rather than manage it as internal infrastructure, white-label VPN solutions represent a genuinely underutilized distribution channel. The economics are favorable enough that the build-versus-buy calculus has shifted considerably.

A fintech super-app building secure connectivity from scratch would need to maintain VPN servers, manage certificates, handle multi-jurisdiction routing, and stay current on protocol evolution (WireGuard vs OpenVPN vs IKEv2, for example). That is a significant ongoing investment for a product team whose core competency is financial services.

A white-label approach offloads that infrastructure while letting the platform own the user experience, the branding, and the data policy. The connectivity layer becomes just another embedded service, like the payment processor or the KYC tool.

The global VPN market is projected to reach $137.7 billion by 2030, growing at a CAGR of 15.3% from 2023. B2B and platform-embedded deployments are a growing share of that figure.

What Embedded Connectivity Is Not

This is a practical distinction, and getting it wrong leads to misallocated security spend.

Embedded connectivity is not a silver bullet for fintech compliance, and it is not a replacement for proper security architecture. A VPN does not make a poorly designed API secure. It does not replace penetration testing, access controls, or incident response planning. What it does is reduce the network-layer attack surface and enforce encrypted communication as a baseline, which is meaningful in a threat landscape where man-in-the-middle attacks and network sniffing remain active tactics.

A report found that 68% of breaches involved a non-malicious human element, meaning a person making an error or falling prey to a social engineering attack. Embedded security that reduces dependency on individual user behavior is therefore genuinely additive to any platform’s defense posture.

PureVPN White Label: Built for This Convergence

As the embedded finance and embedded connectivity markets grow toward each other, the infrastructure choice matters. PureVPN’s white-label VPN solution is designed for businesses that want to offer VPN capabilities under their own brand without building from the ground up.

For fintech platforms, super-apps, and embedded finance providers, PureVPN White Label delivers a ready-to-deploy encrypted connectivity layer. It supports multi-protocol configurations, global server coverage across 88+ countries, and scalable architecture that works whether the client base is 1,000 users or 10 million. The connectivity protection integrates at the platform level, which means it becomes part of the product experience rather than a separate download or optional feature.

The proposition is direct: if a platform is moving money, handling identity, and aggregating services, the network layer cannot be an afterthought. PureVPN White Label treats it as a foundation.

The Competitive Advantage Is Structural

Platforms that integrate embedded connectivity early gain something that is difficult to reverse-engineer later: user trust built into the architecture, not added on top of it.

As embedded finance continues to absorb more of daily financial life and super-apps deepen their hold on user attention across markets, the platforms that survive regulatory scrutiny, avoid breach headlines, and maintain user confidence will be the ones that treated security as a product feature rather than a compliance checkbox. Embedded connectivity fintech is not a niche concern. It is the next structural layer every serious platform needs to get right.