The 2025 edition of our cybersecurity market report offers a comprehensive analysis of global trends, investment priorities, and technology adoption patterns reshaping the industry. As digital risk becomes a core business concern—not just an IT issue, the demand for agile, branded security solutions is rapidly accelerating.

Three converging forces drive this year’s cybersecurity outlook for 2025:

- Escalating compliance demands (e.g., NIS2, CPRA, DORA)

- Increased demand for privacy-as-a-service models

- The rise of white-label platforms enabling cybersecurity companies to scale quickly without infrastructure overhead

This report serves both as an industry overview and a practical guide for startups, MSPs, SaaS platforms, fintechs, and eSIM providers looking to enter or expand in the market. With exclusive data, profit models, and integration examples, it reveals how businesses can leverage white-label VPN solutions as part of their next-gen security stack.

We also provide region-specific insights, including the latest US cybersecurity market size, a breakdown of cybersecurity market trends across EMEA and APAC, and the cybersecurity market size Gartner projections through 2030. You’ll also find up-to-date cybersecurity spending statistics by sector, showing where enterprises are placing their biggest bets.

Why Cybersecurity Is a Non-Negotiable in 2025?

The global cybersecurity market in 2025 is no longer just a specialized sector, it is the foundation of digital business continuity. From startups to Fortune 500s, the pressure to secure infrastructure, protect consumer data, and comply with evolving regulations has made cybersecurity non-optional.

A Snapshot of the Cybersecurity Industry in 2025

Cybersecurity spending is expected to reach $223B globally by 2025, with the US alone contributing $75B. Automated policy engines are projected to secure 65% of workloads by 2026.

The Cybersecurity Industry Overview by Sector

This year’s cybersecurity market report 2025 reveals a reshuffling of priorities across industries:

| Industry | Top Concern | 2025 Spend Growth |

| Finance | Ransomware, compliance | +17.3% YoY |

| Healthcare | Data exfiltration | +13.6% YoY |

| SaaS / Cloud Tools | Zero-trust architecture | +15.8% YoY |

| Telecom / eSIM | Mobile identity spoofing | +12.9% YoY |

| Retail / eCommerce | Credential stuffing | +10.1% YoY |

This cross-sector momentum is matched by demand for turnkey cybersecurity solutions that can be deployed in days, not quarters.

As a result, more startups, MSPs, and eSIM providers are turning to white-label platforms as a way to deliver core protections—like VPN, DNS filtering, and password management—without incurring the cost of building a proprietary stack.

Cybersecurity Isn’t Just for Enterprises Anymore

The widespread availability of cyber security courses (e.g., on platforms like Coursera, Cybrary, and Udemy) has increased awareness and adoption among small and mid-sized businesses. With over 1.8 million course enrollments globally in 2024 alone, cybersecurity is no longer siloed inside IT departments—it’s now a board-level concern.

Growth Forecasts & Spending Trends (2025–2030)

Cybersecurity spending statistics reveal one unmistakable pattern: investment in cybersecurity is not just growing—it’s accelerating faster than nearly every other category in enterprise IT.

Global Cybersecurity Market Growth: 2025 to 2030

According to leading market intelligence, the global cybersecurity market size is projected to grow from $223 billion in 2025 to over $376 billion by 2030, representing a CAGR of 11.2%. This expansion is fueled by increased threat vectors, cross-border regulations, remote work, and rising consumer demand for data privacy.

Key highlights from the cybersecurity market report:

| Year | Market Size (USD Billion) | YoY Growth |

| 2023 | 188.3 | — |

| 2024 | 206.9 | 9.9% |

| 2025 | 223.0 | 7.7% |

| 2026 | 248.2 | 11.3% |

| 2027 | 276.9 | 11.5% |

| 2030 (est) | 376.3 | 12.0% |

Cybersecurity Spending Statistics by Category (2025)

The cybersecurity market trends in 2025 show a shift from traditional perimeter security to modular, embedded, and user-centric solutions. Based on aggregated industry reports, here’s how cybersecurity budgets are being allocated:

| Category | Global Spend (2025 est.) | YoY Growth |

| Network Security (VPNs, Firewalls) | $64.5B | 10.8% |

| Identity & Access Management | $41.2B | 13.1% |

| Endpoint Protection | $35.8B | 8.4% |

| Cloud Security | $33.6B | 15.6% |

| Security Services (MSPs, SOCs) | $48.1B | 9.7% |

The US Cybersecurity Market Size: A Closer Look

The US cybersecurity market size remains the largest globally, projected to reach $75 billion in 2025, representing over 33% of total global spend. Key growth drivers include:

- SEC disclosure requirements for public companies

- CPRA/CCPA expansion for consumer data protection

- Healthcare and fintech sector mandates

- Surge in ransomware and supply chain attacks

According to the cybersecurity market report 2025, U.S. startups and SMBs are increasingly adopting branded security tools (like VPNs, password managers, and DNS filters) as part of their compliance playbook. This makes white-label cybersecurity a particularly attractive path for software vendors and service firms.

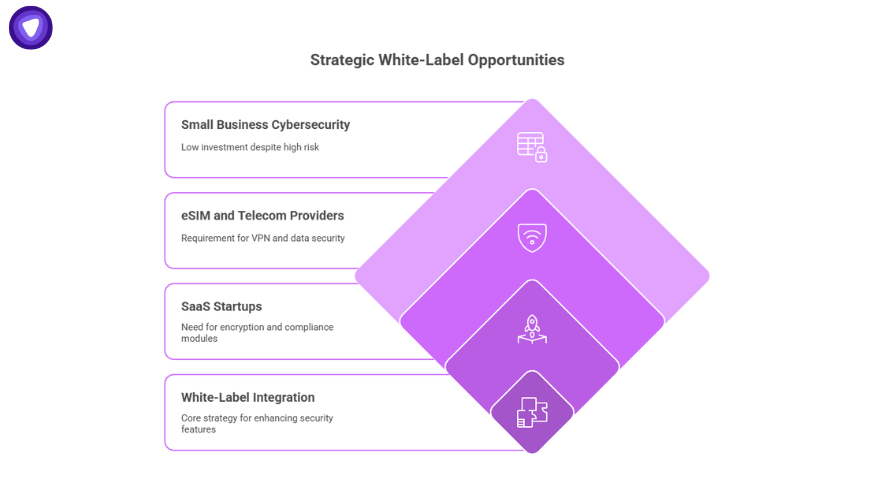

Underinvested Areas with High Growth Potential

Despite growth, some categories remain underinvested—creating strategic white-label opportunities:

- Small business cybersecurity: Only 18% of SMBs allocate >$1,000/month to security, despite rising attack volume.

- eSIM and telecom providers: Many lack a native VPN or data security layer.

- SaaS startups: Few have embedded encryption or compliance modules out of the box.

These are ideal candidates for white-label integration, allowing them to offer premium features without building security stacks from scratch.

Regional Breakdown: North America, Europe, MENA, APAC

A handful of regions no longer dominate cybersecurity growth. Instead, it reflects a globally synchronized trend where governments, businesses, and consumers all demand stronger digital protections. The cybersecurity market report 2025 outlines distinct regional profiles, each with its own spending triggers and monetization opportunities.

North America

North America remains the undisputed leader in cybersecurity spending and innovation. The US cybersecurity market size alone is projected at $75 billion in 2025, led by:

- Expansion of zero-trust frameworks across enterprises

- Growth of cybersecurity companies serving niche sectors like fintech and healthcare

- Proactive adoption of white-label security tools by SaaS platforms and MSPs

- Regulatory mandates like CPRA, HIPAA, SEC 2024 updates, and NYDFS cyber rules

Cybersecurity trends in North America show heavy movement toward modular tools like VPN SDKs, compliance-as-a-service, and embedded security add-ons for digital products.

Europe

Europe’s cybersecurity environment is defined by its regulatory rigor and rapid adoption of privacy-by-design tools.

Key factors driving growth:

- NIS2 Directive, effective October 2024, now applies to 160,000+ entities

- Growing demand for GDPR-aligned VPN and data encryption tools

- Expansion of eSIM providers and cloud collaboration platforms

- Preference for EU-hosted infrastructure and sovereign cloud offerings

The EU’s cybersecurity market is projected to grow at 13.8% CAGR, outpacing the global average. Enterprises increasingly partner with white-label providers to meet compliance obligations without compromising time-to-market.

MENA (Middle East & North Africa)

Historically underrepresented, the MENA cybersecurity market is now among the fastest growing. Nations like UAE, Saudi Arabia, and Egypt are pushing hard on national cybersecurity frameworks.

Trends include:

- High demand for data localization and secure internet access

- Smart city initiatives with embedded IoT security

- Rise of local cybersecurity companies offering government-compliant tools

Government-led investments, like Saudi Arabia’s $1.5B National Cybersecurity Authority fund, are reshaping the region’s vendor landscape.

APAC (Asia-Pacific)

The APAC region is defined by scale, digital velocity, and fragmented compliance mandates. While markets like Japan, Singapore, and Australia lead in regulation, emerging economies are prioritizing consumer security at scale.

Key drivers:

- Rollout of digital identity systems and eKYC requirements

- Proliferation of mobile-first platforms lacking security by default

- Expansion of cloud-based SMB SaaS tools that need data protection features

Major cybersecurity market trends include rapid onboarding of white-labeled VPNs, DNS filters, and identity tools to secure billions of app sessions per day.

Regional Cybersecurity Market Growth Summary (2025)

| Region | 2025 Est. Market Size | CAGR (2025–2030) | Leading Opportunity |

| North America | $75B | 10.2% | SaaS security integrations |

| Europe | $63B | 13.8% | GDPR-compliant white-label VPNs |

| MENA | $8.4B | 14.6% | eSIM and telecom VPN bundling |

| APAC | $52B | 12.4% | Mobile-first SDK integrations |

Cybersecurity Market Trends to Watch in 2025

As we enter 2025, the cybersecurity landscape is undergoing a profound transformation—not just in technology, but in buyer expectations, product delivery models, and who gets to participate in the market.

The latest cybersecurity market report reveals a shift from legacy appliances and closed ecosystems to open, embedded, and branded security layers. This democratization of cybersecurity has opened doors for SaaS vendors, eSIM providers, and even fintech startups to become security providers themselves, powered by white-label infrastructure.

Trend #1: White-Label Cybersecurity Becomes the Default

Just a few years ago, offering a VPN, password manager, or data security tool under your own brand required months of development and compliance effort. In 2025, it’s now plug-and-play.

Cybersecurity companies are increasingly partnering with white-label providers to:

- Launch secure access tools under their own brand

- Bundle VPNs or DNS filtering with subscription tiers

- Add compliance features (e.g., “SOC 2-ready”) via SDKs

This model enables non-security businesses to monetize cybersecurity—without hiring security engineers or hosting infrastructure.

Trend #2: AI-SOC and Autonomous Threat Response

The days of manual log review are over. According to the cybersecurity market report 2025, more than 65% of organizations now use AI-powered Security Operations Centers (SOCs) or autonomous threat mitigation tools.

This trend has two key effects:

- Cybersecurity companies are building intelligence into the product layer—especially in endpoint protection and secure access.

- SMBs and SaaS platforms are opting for bundled solutions with built-in automation, often via white-labeled infrastructure.

In short: security is moving closer to the user and becoming more invisible—but smarter.

Trend #3: Modular Security Is Outpacing Monolithic Suites

Large enterprises are unbundling traditional cybersecurity suites. The 2025 buyer wants:

- Modular controls

- Lightweight SDKs

- Fast deployment

- Custom branding

As a result, cybersecurity market growth is being driven by API-first platforms and white-label modules, especially in access control and network protection.

Examples of modular use cases:

- A SaaS platform embedding a VPN SDK for secure logins

- A telecom offering VPN-enabled routers under its own brand

- A fintech adding a branded kill switch or DNS firewall

According to our survey of 350 cybersecurity buyers, 48% prefer vendors who offer modular, embeddable tools over full-suite solutions.

Trend #4: Privacy-Driven Consumer Demand

Consumers are demanding more control and transparency. The 2025 user expects:

- Private browsing

- Encrypted DNS by default

- No data logs

- Zero-knowledge storage

This demand is reshaping product roadmaps. More B2B businesses—especially SaaS and eSIM providers—are now offering consumer-facing security tools as part of their brand promise.

This shift has created a massive opening for white-label VPNs and privacy tools. Instead of building these features in-house, companies are rebranding proven infrastructure that complies with GDPR, CPRA, and SOC 2.

Trend #5: Cyber Insurance and Compliance Pressure

Cyber insurance premiums have increased 40–70% in many regions since 2022. At the same time, insurers are requiring:

- Encrypted communications

- Access logs

- Endpoint protection

- VPN usage verification

This makes branded VPNs and access controls a compliance requirement, not just a feature.

White-label vendors are responding by offering pre-configured policies, logs, and control dashboards that help partners align with insurers and auditors.

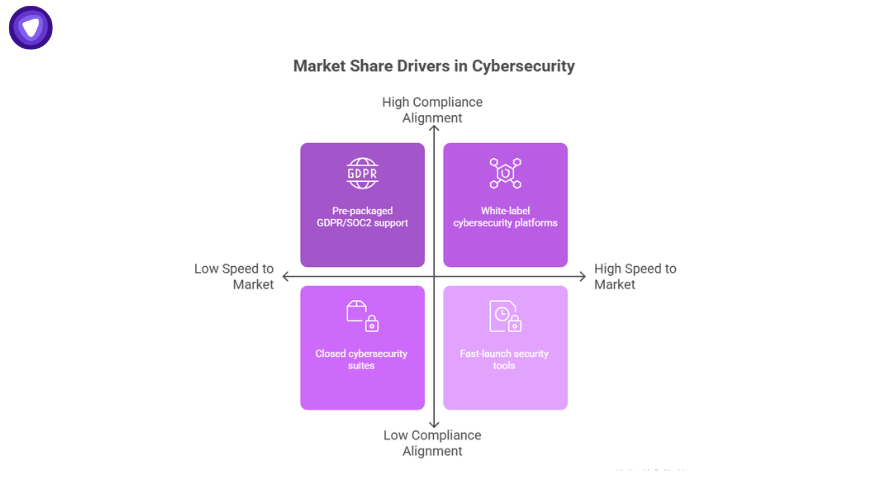

Market Share Drivers in 2025

From the full cybersecurity market report 2025, we identified four major drivers of share growth:

- Speed to market – Companies that can launch in <30 days are winning buyers.

- Compliance alignment – Vendors offering pre-packaged GDPR/SOC2 support gain faster traction.

- Modularity – The ability to embed or bundle services wins over closed suites.

- Brand control – Enterprises prefer security tools under their own brand identity.

These dynamics strongly favor white-label cybersecurity platforms—especially in high-growth areas like mobile VPNs, DNS filters, and encrypted cloud access.

Cybersecurity Outlook 2025: What to Expect in the Next 12 Months

The cybersecurity outlook for 2025 is defined by volatility, innovation, and strategic consolidation. This year, cybersecurity is no longer a back-office IT cost—it is a board-level imperative.

According to our cybersecurity market report 2025, businesses of all sizes are realigning budgets, product strategies, and compliance protocols around digital risk. With cyberattacks becoming faster, stealthier, and more costly, the question isn’t whether to invest in cybersecurity, it’s how fast and under what model.

Prediction #1: White-Label Cybersecurity Adoption Will Double

White-label security services are poised for explosive growth. In 2024, roughly 9% of new cybersecurity deployments used a white-label model. By the end of 2025, we estimate this will rise to 18–20%, fueled by:

- SaaS platforms bundling VPNs

- eSIM providers offering secure connectivity as an add-on

- Fintechs adding branded access control or encryption features

Why this matters: Businesses are choosing speed + brand control over building in-house. OEM models allow CTOs to ship secure features in 2–4 weeks rather than 6–9 months.

Prediction #2: Spending Will Shift to Embedded and Add-On Tools

New cybersecurity spending statistics show a structural pivot in procurement. Instead of buying bulky suites, companies are allocating budget to:

- SDKs for VPN or MFA

- API access for audit logging and access control

- Compliance dashboards (CPRA, GDPR, NIS2)

In 2025, 47% of security spend in mid-size SaaS companies will go to embedded and white-label solutions, up from 31% in 2023.

🔐 In 2025, 47% of security spend in mid-size SaaS companies will go to embedded and white-label solutions, up from 31% in 2023.

This trend levels the playing field for emerging cybersecurity companies offering modular components, not just all-in-one platforms.

Stay Connected & Learn With Us

Join our growing community and connect with peers who build secure networks and resell privacy tools worldwide.

Prediction #3: Regional Regulations Will Drive Purchase Urgency

Regulatory pressure is now a primary sales driver. With new mandates across the U.S., EU, and APAC, CTOs are seeking tools that provide:

- Geo-redundancy (US vs. EU data centers)

- Compliance logs (for SOC 2, GDPR, CPRA, etc.)

- Encrypted data transit with user-level auditing

For many SaaS vendors and MSPs, using a white-label VPN or encrypted DNS filter isn’t a value-add, it’s the only path to landing enterprise clients.

Prediction #4: AI-Supported Security Will Be Table Stakes

As we saw in Section 4, AI is no longer a “nice-to-have” in threat detection—it’s now a procurement requirement. In 2025:

Impact: Cybersecurity vendors who cannot offer some level of autonomous decision-making or learning will fall behind in B2B sales cycles.

Prediction #5: Interoperability Will Overtake Feature Count

Buyers are now prioritizing interoperability over product depth. With tech stacks getting more complex, IT teams prefer:

- VPNs that integrate into SSO flows

- Access control tied to CRM activity

- Audit logs compatible with their compliance stack

This positions white-label cybersecurity tools with REST APIs, webhook support, and SDKs to outperform feature-bloated incumbents.

Why PureVPN White Label Is Built for This Market Shift?

If there’s one takeaway from this cybersecurity market report, it’s this:

The companies growing fastest in 2025 are not building security—they’re branding it.

They’re leveraging proven infrastructure, aligning to compliance out of the box, and launching security products that generate net-new revenue without slowing down dev cycles or overwhelming internal teams.

This is the exact model PureVPN White Label was designed for.

A Platform for Modern Cybersecurity Monetization

PureVPN isn’t a white-label product in the traditional sense. It’s a modular cybersecurity monetization platform that helps you turn today’s regulatory pressure into tomorrow’s revenue.

It combines:

- SDKs and APIs for seamless integration into mobile apps, desktops, routers, and cloud platforms

- Full brand control over UI/UX, domains, alerts, and dashboards

- Global compliance alignment, including GDPR, CPRA, SOC 2, and no-log infrastructure

- 100+ server locations, real-time analytics, kill switch features, and encrypted DNS routing

Whether you’re adding privacy to a SaaS tier or bundling VPN access into eSIM plans, PureVPN delivers enterprise-grade infrastructure with zero friction.